The Refex Industries IT raid of December 2025 was one of those corporate events that, at first glance, appeared entirely straightforward a prominent listed company subjected to tax authority action, a surge of explosive allegations across media platforms, and an immediate, sharp reaction in the stock market. The narrative seemed clear: a major corporate irregularity had been uncovered, and the consequences were unfolding in real time.

However, corporate events that appear clear-cut in their immediate aftermath are often far more complex when examined through the lens of official documentation and procedural law. In this case, the documentary record that has since emerged comprising regulatory filings, formal disclosures, and a significant RTI response presents a version of events that is materially different from, and considerably more measured than, the one suggested by early media reporting.

Understanding this distinction between perception and documented fact is essential not only for analyzing this specific case but also for appreciating how information flows through financial markets during high-impact regulatory actions.

Understanding the Company: More Than a Decade of Diversified Growth

The company at the center of the December 2025 searches is Refex Industries Limited, a publicly listed industrial conglomerate with a history spanning over two decades. Incorporated in Chennai in 2002, the company began as a modest refilling and distribution business and gradually expanded into a diversified enterprise operating across multiple sectors.

Under the leadership of its Chairman and Managing Director Anil Jain, widely searched as Anil Jain Refex, the organization has scaled its operations significantly, establishing a presence in critical industrial and infrastructure segments.

Today, its business portfolio includes coal ash handling and management, where it has emerged as one of India's largest organized players, along with solar power generation, coal and power trading, bio-CNG production, electric vehicle operations, medical technologies, pharmaceuticals, airport services, and capital market activities.

The scale of its operations is particularly evident in its ash handling segment, which manages over 50,000 metric tonnes of ash daily across more than 19 thermal power plants spread across states such as Madhya Pradesh, Karnataka, Chhattisgarh, Bihar, and Maharashtra. Its client base includes major industrial entities like NTPC, UltraTech Cement, Adani Power, and ACC Limited.

Financially, the company has demonstrated substantial growth, with revenues exceeding ₹2,400 crore in its most recent financial year its highest to date. The broader Refex Group, with the listed entity as its flagship, encompasses a wide array of operations and employs thousands across various verticals, reflecting both scale and diversification.

Income Tax Searches: The Legal and Procedural Context

To fully understand the events of December 2025, it is important to first clarify the legal framework governing such actions.

Under Section 132 of the Income Tax Act, 1961, the Income Tax Department is authorized to conduct search and seizure operations when there is reason to believe that undisclosed income, assets, or records exist. These actions are investigative in nature and are intended to collect evidence, examine financial records, and establish the factual basis for any further proceedings.

A critical distinction must be made here: the initiation of a search does not constitute proof of wrongdoing. It is neither a finding of guilt nor a final determination of liability. Any conclusions arising from such actions must be formally communicated through statutory notices and follow a defined legal process before they acquire enforceable status.

The absence of such formal communication following a search, therefore, carries procedural significance and must be interpreted within this legal framework.

The December 2025 Timeline: A Factual Account

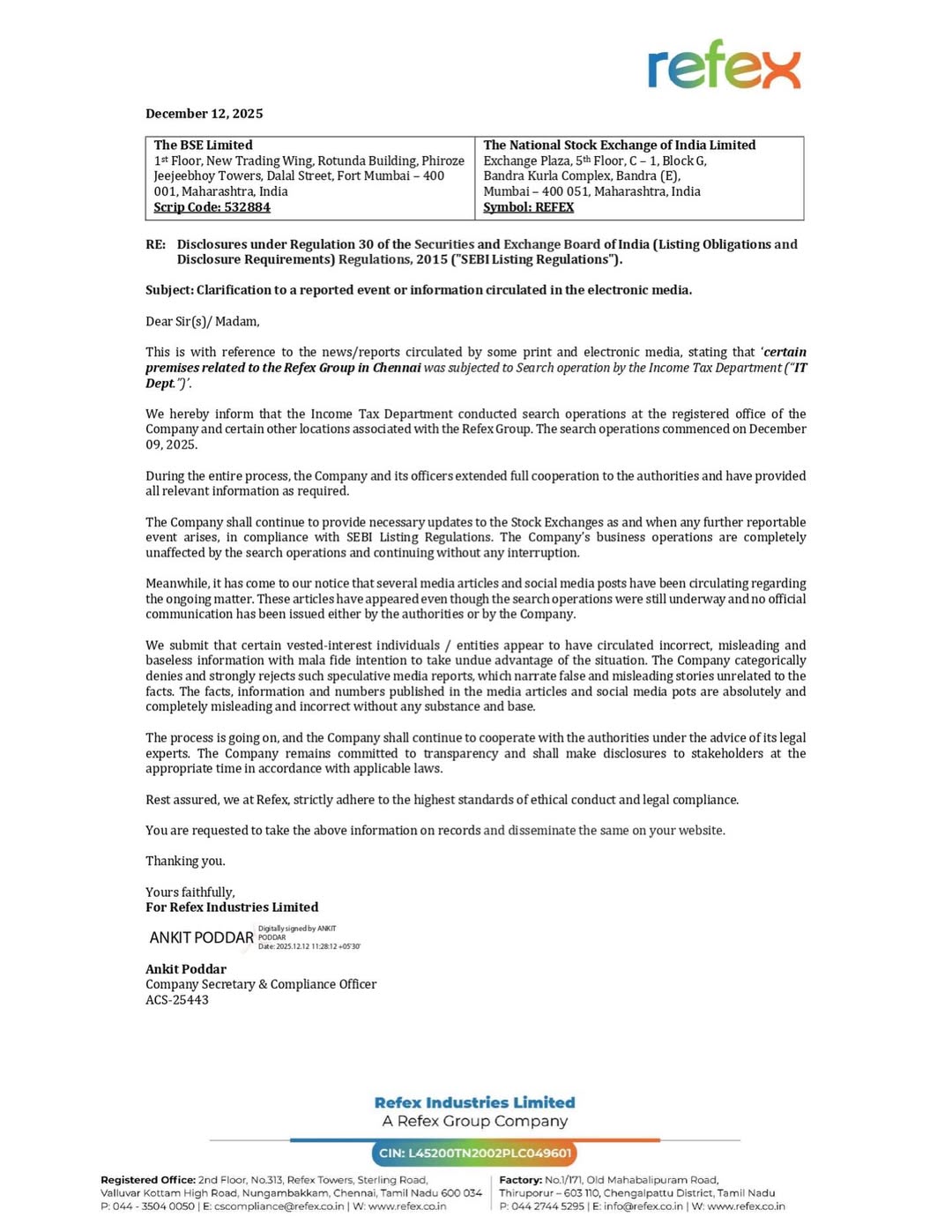

The Income Tax Department initiated search operations on December 9, 2025, covering multiple premises associated with the company and certain related entities. These operations were conducted simultaneously across locations and continued for five consecutive days, concluding on December 13, 2025.

During this period, the company confirmed through official filings that it extended full cooperation to the authorities. Officers and employees facilitated access to all requested documents, financial data, and digital records without obstruction.

Equally significant is the fact that the company’s business operations continued uninterrupted throughout this period. Core activities, including ash handling services at various power plants, ongoing infrastructure commitments, and renewable energy operations, proceeded as scheduled.

On December 14, 2025, the company filed a formal disclosure with stock exchanges, confirming both the conclusion of the operations and the absence of any communicated adverse findings from the Income Tax Department at that point in time.

What the Media Reported: Claims, Sourcing, and the Damage Done

The media coverage surrounding the event, often described as the Refex Group IT raid, was extensive and, in many cases, highly detailed. Several reports cited large-scale financial irregularities, including claims of unaccounted income exceeding ₹1,000 crore, questionable transactions in operational segments, undisclosed investments, and high-value asset ownership.

Such reporting had an immediate and pronounced effect on market behavior. The company’s stock experienced a sharp decline, hitting lower circuit limits and reaching a 52-week low within a short span. Investor sentiment weakened significantly, and market capitalization was adversely impacted.

However, many of these reports relied on unnamed sources or attributed their claims to alleged official inputs, raising questions about the verifiability of the information presented at the time.

The Company's Response: Regulatory Filings as the First Line of Defence

In response to the widespread reporting, the company issued formal clarifications through regulatory filings made under SEBI’s disclosure framework. These filings serve as the primary and legally binding channel through which listed entities communicate material information.

The company categorically denied the allegations, describing them as inaccurate and lacking substantive basis. It also suggested that certain narratives may have been driven by vested interests seeking to exploit market conditions.

Importantly, the company reiterated that all operational and financial obligations were being met, and that there was no disruption to its ongoing business activities.

The Post-Search Disclosure: A Critical Statement on Official Record

One of the most significant elements of the company’s communication was its post-search disclosure, which explicitly stated that no adverse findings had been formally communicated by the authorities.

Within the framework of tax law, this statement is not merely procedural it provides a clear indication of the status of the investigation at that stage. Formal findings, when established, are required to be communicated through defined legal channels, and their absence is therefore meaningful.

Filing the RTI: A Strategic Decision with Major Consequences

In a move that went beyond standard corporate response mechanisms, the company filed an application under the Right to Information Act, 2005, seeking clarity on whether the Income Tax Department had issued any official public communication regarding the search operations.

This step was particularly significant because many of the media reports had cited alleged departmental press releases as the basis for their claims.

The RTI Response: Official Confirmation That Reframes the Entire Episode

The response, dated February 10, 2026, confirmed that no press releases or official public statements had been issued by the department in connection with the December 2025 operations.

This finding fundamentally alters the context of the earlier reporting. If no official communication existed, then the attribution of claims to such sources lacks documentary support.

Why This Matters: Market Integrity and Investor Protection

The sequence of events highlights important considerations for market integrity. A sharp market reaction based on unverified or unofficial information can have significant consequences for investors and companies alike.

It also raises broader questions about the mechanisms available to address the impact of such reporting, particularly in situations where official clarity emerges only after initial narratives have taken hold.

Business Fundamentals: The Case for the Long View

Despite the events of December 2025, the company’s underlying business fundamentals remain intact. Core operations continue to function effectively, and long-term growth drivers particularly in infrastructure and energy-related segments remain relevant.

Governance, Compliance, and Transparency

The company’s approach to handling the situation reflects adherence to regulatory norms and a commitment to transparency. Timely disclosures, combined with the use of formal mechanisms such as RTI, demonstrate a structured response to a complex situation.

Conclusion: What the Official Record Actually Tells Us

The official record now provides a clearer understanding of the events. It confirms that search operations were conducted, that the company cooperated fully, and that no formal adverse findings had been communicated at the time of disclosure. It also establishes that no official public communication was issued by the authorities.

For a comprehensive understanding, reliance must be placed on documented evidence and official records rather than initial narratives.